I’ve had a lot of people ask for an update to my original article.

Instead of updating the original chart, I wanted to provide you with a

calculator for you to use/share/edit. It’s available in GoogleDocs here:

Coinpot Faucet Calculator.

The

model is very simplistic, but gives you an idea for what you can earn

in one year. It then gives you the ability to see how much that would be

if prices go up by the end of the year. Finally, it provides a way to

see how much the crypto made from one year using Coinpot will be worth

based on growth rates like the ones we’ve seen over the past 10 years.

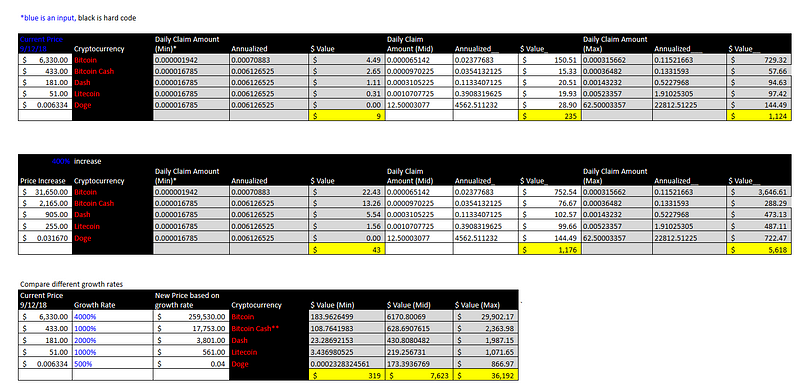

(Click here for a snapshot of historical prices from 2013. Bitcoin is up over 4000% while Litecoin is up over 1000%.)

The

spreadsheet provides a calculator for each faucet based on current

claim rates. The final spreadsheet is a chart (shown below). It provides

a summary of all three calculators.

Keep

in mind, the calculator only looks at one year. It also does not

include the mystery bonus, offer bonus or mining bonus. I wanted to err

on the side of extreme caution, so each calculator only assumes one

claim per day.

The

base rate assumes no referrals, 1 claim per day and an average of 50%

loyalty. The mid rate assumes 100 referrals, 1 claim per day and an

average of 75% loyalty. The max rate assumes 500 referrals, 1 claim per

day and an average of 100% loyalty. Note, the max rate is not a maximum.

It is only used as a max case. Theoretically, there are no limits.

I can personally attest to the mid case. I have around 80 active

referrals and only make one claim per day. I’m on track to make more

than $235, but that’s because the values above don’t include the mystery

bonus or Coinpot tokens, which add up. On average, I get around 3000

tokens per day. Again, I wanted to be very conservative here so those

tokens are not included.

You

can play with a number of scenarios around loyalty and referrals. While

I don’t want to dissuade anyone from doing this, I think referral activity is critical.

This way, even if you can’t make daily claims, you’ll still have a

growing Coinpot. If you don’t get referrals, this isn’t going to payoff.

So, I’ve created a contest for the best referral idea.

One final word

A

chap recently asked me how to convince people that this isn’t a scam.

My answer is: you can’t. But you CAN point out that a scam generally

requires you to spend money. Coinpot will never ask you for money. The

only thing you are required to give them is an email address.

Also,

remember that bitcoin is still the world’s fastest growing asset. And,

Coinpot is a great way to “get your feet wet” (as one person commented)

in the world of cryptocurrency. The learning curve can be steep for

some. It’s also a great way to earn bitcoin without having to worry

about price fluctuations, providing ID or paying any fees. When the

price goes down, the claim is higher. And since I know the price is

going back up, it’s an opportunity.

Finally,

the goal here is not to make a quick buck. You will be disappointed if

that’s your goal. This is not a get rich quick scheme. Put simply, this

is a great way to earn small amounts of what I believe will be the next

reserve currency for the world. It may not be worth much now, but the

goal is to hold onto this asset for the long-term (at least 10 years).

All you’re risking is your time. Even if you just do it for one year,

you’ll always have it and its value will grow over time.

You

can learn a great deal by listening to the "public" speeches given by

Fed leadership. It's one thing to give testimony on Capital Hill, it's

quite another to give a speech in front of people that actually know

what you're talking about. In this speech, Gruenberg, the Chairman of

the FDIC, discusses the actions taken over the past 10 years to ensure

against another "Great Recession".

He discusses the

establishment of the Dodd-Frank Act and the authority it gave the FDIC

to manage the orderly failure of banks in times of crisis. Among other

things, the new authorities gave the FDIC:

The ability to place the financial firm, including its holding company, into a receivership process; An Orderly Liquidation Fund to assure liquidity for the orderly wind down and liquidation of the failed firm; Authority to impose a short stay on derivatives contracts; and The ability to coordinate with foreign authorities in the case of a firm with global operations.

"The

progress has been substantial and I believe not well appreciated,"

Gruenberg concludes. What hasn't he and his team been appreciated for?

The Evolution of the Living Will Process

As

a way to create a framework around an orderly bank liquidation, the

FDIC created the living will process. According to Gruenberg, the living

will "required both the Federal Reserve and the FDIC to consider the

objectives of the process, the standards and the guidance that would

need to be provided to the firms to achieve the objectives, and the

means of engagement with the firms to assist them in following the

guidance". This process required banks to provide a description of the

following:

The firm’s strategy for orderly resolution in bankruptcy during times of financial distress; The range of actions the firm proposes to take in resolution; Liquidity and capital needs and resources of the firm; A description of the firm’s organizational structure, material entities, interconnections, and interdependencies; and The firm’s corporate governance process.

The

only thing that really matters here is liquidity. With the right

liquidity and capital resources, any crisis can be avoided or at least

pushed off, but for how long?

The truth is, none of these

changes would have saved Lehman Brothers or Bear. None of these

resolutions would have made AIG confess to creating bad securities. The

truth is, everything happened exactly how the banks wanted it to happen.

They got a huge bailout, 10 years of free money, and trillions in

reserves at the Fed. To top it all off, Dodd-Frank approved a resolution

to pay banks for those reserves. Who pays the interest? We do. The

American taxpayer. We don't control rates or the amount of reserves held

at the Fed, but we have to pay whatever rate the Fed sets on those

reserves. Sounds fair. This is why people are gravitating toward Bitcoin

and precious metals.

In other news, Nowcast is a forecast of the upcoming GDP announcement. It was

updated and revised down to 3.11%. The leading causes are due to a

decline in:

capacity utilization,

industrial production,

general business conditions (as reported in a daily brief last week); and,

retail sales.

In

other words, all things driven by consumer demand are starting to

decline, while anything driven by debt (inflation, pricing and

housing) are on the rise.

The Empire State Manufacturing

Survey/Business Leaders Survey included a supplemental survey on wages, a

critical piece of the consumer demand equation. Wages are of key

interest because without wages, GDP will continue to fall -- not

everyone has access to massive amounts of debt. What does the survey

show? Job openings are taking longer to fill, manufacturers are hiring

more, and starting pay is going up. Will it be enough to impact

earnings? My guess is no. Why? Wall Street doesn't like wage increases.

This post is about the September 2019 bank bailout related to the repo market. It will provide answers to the following questions: 1) what is a repo? 2) how are banks being bailed out? 3) why is the bailout happening? 4) what does it mean for the great value migration? 5) what can you do?

First, let's understand why the bailout is so important. Why is the September 2019 bailout so important? The September 2019 bailout is important because the Federal Reserve is pumping money into OUR economy, non-stop ($260 billion in assets to the

Fed’s balance sheet since mid-September). Yet, we have heard little about this. When the Fed bailed out banks in 2008, it was alarming. Everyone knew about it, today, only the business community is covering it.

Why is this bailout happening? A large bank probably went bust in September. We'll never know which one because it was "bailed out". How are banks being bailed out? The Federal Reserve is pumping large amounts of money into the economy every night through an overnight lending program they have set up for banks. For a small fee, banks can make sure they have enough cash to stay open tomorrow. If there's a large demand for overnight funds, the fee goes up. In September, the fee went up so much due to the demand for overnight funds, the Fed had to step in to assist. In other words, the Federal Reserve had to step in to guarantee funding for any bank that needed it. What is a repo? A repo is short for repurchase agreement. This is the name of the banking product used to make overnight loans. In the same way that a mortgage is the name of the banking product used to make loans for houses, a repo is the name of the banking product that is used to make overnight loans. So, when people talk about the Fed bailing out the repo market, they are referring to another massive bailout for the loan market, except this time it's the overnight lending market (repos) not mortgages (mortgaged backed securities).

What is the size of the repo market?

The repo market is huge. According to the Securities Industry and

Financial Markets Association, the average daily repo volume in 2018 totaled nearly $2.2 trillion. So the repo market – with about $2.2 trillion outstanding – blew up

in mid-September and repo rates spiked to 10%. Then, the Fed stepped

in with a bailout. Why is the Fed allowed to do this? In 2008, it was decided that certain banks were deemed "too big to fail". As a result, the Fed has the precedent authority to bailout any large bank. So, we'll never know what large bank was bailed out this time (perhaps JP Morgan), but we do know that it took a massive amount of cash to do so. We also know that the Fed is playing this by ear. In fact, they have no idea what's happening. The new Federal Reserve Chair has openly stated his ignorance regarding next steps. This is even more evident in the announcements made by the Fed's trading desk. Brad Huston on Twitter provides a good overview of the Fed's announcements through Twitter below.

High Level Overview We got in the weeds there so let's pan out for a moment.

What are the main takeaways from this? 1) The Fed just bailed out another massive bank (at least one). And, it will continue to do so until the U.S. dollar collapses. 2) The Federal Reserve will do everything it can to prevent a recession. This is a new development in economic theory. It used to be that recessions were an inevitable part of a market economy. Now, they aren't allowed. What does this mean from an investment perspective? Ultimately, it means that if you're just listening to MSM, you could be on the wrong side of many trades. It's time to take all the cash you can afford to lose and invest it in the stock market. The Federal Reserve, through its repo program (lender of last resort) and quantitative easing program (buyer of last resort), will continue to support or bailout any issue related to the stock market. The Fed knows the stock market is the primary indicator of economic health for most folks, so it will continue to prop it up by buying assets. This is why the Fed and central banks across the world are pushing rates lower (see article on negative rates below). All that cash has to go somewhere, and it's going into the market. The best thing you can do for your portfolio is buy on dips. How does this relate to the Great Value Migration from the dollar to bitcoin? While it's time to invest your "extra" cash in the stock market (especially the ones that make up the major averages (DJIA, S&P, NASDAQ)), it's also time to start putting the cash that you can't afford to lose in safer places. This means assets that aren't associated or "backed" by a certain institution or counterparty, i.e, real estate, bitcoin, precious metals, artwork, jewelry. That way, if the market fails, it won't impact the intrinsic value of the asset you hold. What is Counterparty Risk & Why You Don't Want It?

In the financial world, "backing" is referred to as a "counterparty". A counterparty can be a bank, the Federal Reserve or any institution that's willing to "back" an asset. So the risk associated with buying assets that are backed by a certain institution is referred to as counterparty risk. Almost all assets in the market, except for the ones listed above, gain value from the counterparty backing. The dollar is backed by the Federal Reserve. Stocks are backed by the company. Mortgaged backed securities are backed by the people paying the mortgages. Repos are backed by the lender. Bitcoin is backed by the people that use it (no counterparty). Gold is backed by its own intrinsic properties (no counterparty).

The great value migration refers to the migration from currency "backed" by central bankers to currency with no counterparty risk, like bitcoin and gold. Get ready. We're crossing the Rubicon. If you're hungry for more on this subject I recommend:

"The final rule removes references to external credit

ratings and replaces them with appropriate standards of

creditworthiness."

In other words, as long as a bank makes under $1 billion in total assets it doesn't need to reference external credit ratings in order to label an asset or security as "investment grade". These classifications are used for capital allocation and pledged assets. The rule reduces the need to classify assets as investment grade with a much lower bar -- as of this ruling "An entity has adequate capacity to meet

financial commitments if the default risk is low, and the full and

timely repayment of principal and interest is expected."

The rule also "adds cash to the list of assets eligible for pledging

and separately lists Government Sponsored Enterprise obligations as a pledgeable asset category."

So mortgaged backed securities are now considered pledgeable assets as well as cash? And, if you have cash, why do you need to pledge assets?

The report

reveals that total household debt reached a new peak in Q4 of 2017, rising $193 billion to reach $13.15 trillion. Balances

climbed:

1.6% on mortgages,

0.7% on auto loans,

3.2%

on credit cards; and,

1.5% on student loans.

This adds to the market's general instability, but we're not hearing anything about that from the Fed. It's also important to remember that debt is a form of inflation. It's essentially the creation of money out of nothing. Due to quantitative easing, banks have an unprecedented level of capital to "lend" and it's pumping all that "fake cash" into the market every day via mortgages, auto loans, credit cards and student loans. Asset values are the highest they've been in years, far surpassing what they were in 2007, jut prior to the Great Recession. Gas prices have been on the rise since July of 2017, still inflation is low and steady. Clearly there's some manipulation at play.

According to the Empire State Manufacturing Survey, a monthly survey of manufacturers in NY conducted by the Federal Reserve, the general business conditions index fell five points to

13.1.

This suggests a "slower pace of growth than in January". This at a time when the stock market was setting new highs. Perhaps the most notable takeaway is a remark about input prices and prices paid which confirms a theory of higher inflation. According to the report, "Input price increases picked up noticeably, with the prices paid index

reaching its highest level in several years." The highest level in several years is quite significant. So companies are paying more for inputs and they are charging more for products and services. I wonder who is paying for those products and services?

According to the Fed, there's been a marked increase in the number of jumbo loans on the market today. This isn't surprising because banks have an unlimited amount of capital to lend due to quantitative easing and the $2.2 trillion sitting in reserves at the Fed. This post shows how "the

supply of jumbo mortgages has improved in recent years as banks have

become more willing to take on mortgage credit risk on their own balance

sheets".

Final Thoughts: The Fed has been waiting on inflation to go above 2% to raise rates. The truth is, inflation has been over 2% since 2008. It went up and never really came back down. Meanwhile, the Fed kept rates artificially low and corporations have taken advantage of the loophole by using stock buybacks to artificially push up earnings. Now it's too late to raise rates, the economy is about to crash on its own.

Everyone wants to know when the price of Bitcoin is going back up. In this very brief article I'm going to give you three reasons why the price of Bitcoin is about to go up and well past $20Kby the end of the year.

Reason #1: The price of Bitcoin and cryptos in general falls every year in Q1. Each year, the price rebounds and soars by the end of the year.

As you can see from the charts above, this is a normal trend for Bitcoin and one that the community has come to expect.

Reason #2: Despite the call for regulation by central banks, nation states are starting to realize their own power. While the SEC and CFTC battle over who gets to regulate cryptocurrency, Arizona just passed a bill allowing it as a form of payment by the Department of Revenue. In other words, you will be able to pay your Arizona taxes in Bitcoin. There's also a resolution passed in Congress calling for a pro-bitcoin national policy. When/if that resolution gains traction, the price of Bitcoin will soar.

Reason #3: Third and perhaps most importantly, hedge funds and other large institutional players are just now getting into the market. They could not enter the market prior to Bitcoin futures which started in December 2017. Below is one of my favorite videos in support of this, hedge fund manager clearly explains what institutional players are doing right now.

It might take six to eighteen months, but Bitcoin is a much more valuable way to store your digital currency. Remember, only 9% of the world's currency is physical, the rest is digital. Institutions get it and they're getting on board.

Final thoughts: Bitcoin is extremely volatile. For this reason, you don't want to buy at the highs, but rather the lows. Bitcoin is officially in a low cycle and now is a great time to buy. If you don't buy now, save up to buy next year at this time.

Where to buy? You can buy Bitcoin from an exchange (Binance or Local Bitcoin) to hold yourself or you can purchase an investment product, like an IRA. Bitcoin IRAs have the same tax treatment as traditional IRAs.

This is one of those articles the Federal Reserve releases that has absolutely no application. It's asking if increased capital requirements help banks to reduce the amount of risk they take. The answer is OF COURSE!!!!! Are you kidding me?

This is like asking if someone feels the same if they lose their money or someone else's money. That said, I think this article has more application than the title gives it credit for. Here's a quick excerpt from the article:

Excessive risk-taking by banks has long been a paramount concern of

regulators. The basic problem arises in part due to misaligned

incentives; under the current limited (single) liability

structure, shareholders of a failed bank can lose no more than their

initial investment. With this limited skin in the game, bank

shareholders’ private incentives may lead them to take more risk than is

socially optimal. If, by contrast, shareholders were liable for the

entirety of a bank’s losses, their private risk-taking decisions may be

more aligned with socially optimal risk‑taking.

So, instead of looking at this as a consideration for banks, let's extend it. This should be a consideration for all stocks. Perhaps the issue with the corporate state is that the shareholders don't have any personal liability. They are limited in the amount they can lose. What if the shareholder had to worry about being liable for legal or environmental issues? What if the shareholder had to worry about being sued for the corporation's irresponsibility? I suppose a lack of earnings equates to a sell-off, which is the ultimate punishment for the corporation.

Final thoughts: This article does nothing but shed light on the fact that we still have an incredible amount of power over the corporate state. Anything that can hurt earnings is a threat to the corporate state, including its own hubris. Couching gambling schemes in terms of limited liability structures doesn't hide what's happening. If anything, it is a concession to the system's vulnerabilities.

______________

The Overnight Bank Funding Rate currently stands at 1.42%. Do not be confused. This rate is based on the interest rate on excess reserves (IOER rate), which is not the same as the interest rate on required reserves (IORR). Currently, both rates are the same, however (you can view both rates here)

If you're old like me, you remember when the rate was referred to as the fed funds rate. The name was changed when banks were given the ability to charge interest on reserves in 2008. Once this deal was made, the Fed started giving out "reserves" like candy in a scheme referred to as quantitative easing. Today, over $2.2 trillion sits in reserves at the Fed and we (the United States) are paying interest on all those reserves, both at the IOER and the IORR.

The overnight bank funding rate is reported every day. It will never be higher than the rate banks can get from leaving money at the Federal Reserve (IOER or the IORR).

Final thoughts: Every now and then I like to revisit this issue of rates. I hear people wondering if the Fed is going to raise rates and I wonder if they understand what's really going on. Ultimately, the real reason why the Fed is going to raise rates has very little to do with the state of the economy. And, the higher rates go, the more banks get paid. The issue for banks is that inflation is a four letter word. It means lenders will be paid back with less money. If you own $100,000 on your home, and the value of the dollar tanks by 50%, you still owe 100,000 of those dollars, but they're only worth $50,000. Inflation is great for borrowers. So, the game the Fed has to play is -- how do we make sure people still believe in the value of the dollar while raising rates? It has nothing to do with cooling off the economy.

___________

The next article is about Deutsche Bank. The bank will have to pay $3.7 million to customers for misleading them about mortgage backed security prices. What's interesting to me is that this is supposed to be a fair settlement.

To settle the charges, Deutsche Bank agreed to reimburse customers the

full amount of firm profits earned on any CMBS trades in which a

misrepresentation was made. According to a payment schedule in the

order, Deutsche Bank will distribute more than $3.7 million. Deutsche

Bank also agreed to pay a $750,000 penalty. Solomon agreed to pay a

$165,000 penalty and serve a 12-month suspension from the securities

industry.

$3.7 million is nothing in the trading world. We are supposed to believe this is the full amount of the profits made? What's funny is that the SEC apparently believes it. They also think that a 12-month suspension from the securities industry and a $165K penalty is going to stop this kind of activity. The penalty is nothing compared to rewards, even if you do get caught. Final thoughts: As I've said before, the SEC has been rendered toothless over the years. What's funny is that the very banks that gutted the SEC's power are asking for its protection against Bitcoin. Good luck with that.

__________

As an extension of what's going on at the SEC gutting, I think it's interesting that the SECs budget request is 3.5% higher than it was last year.

In order to keep up with the rapid pace of technology advancement in the

areas the SEC regulates, the request seeks a $45 million increase in

funding for information technology enhancements to support the agency’s

cybersecurity capabilities, risk and data analysis, enforcement and

examinations, and automation of business processes. The fiscal year 2019

budget request level is a 3.5 percent increase over the fiscal year

2018 budget request of $1.602 billion.

The total request is for $1.658 billion.

__________

On Monday, the SEC launched the Share Class Selection Disclosure Initiative (SCSD) to encourage self-reporting. The SEC has no way to enforce this really -- how can they enforce fiduciary responsibility when its antithetical to capitalism? So they've created a hotline to encourage self-reporting. This is also funny. Here's an excerpt that sums up the effort:

The Commission has long been focused on the conflicts of interest

associated with mutual fund share class selection. Differing share

classes facilitate many functions and relationships. However, investment

advisers must be mindful of their duties when recommending and

selecting share classes for their clients and disclose their conflicts

of interest related thereto. In the past several years, the Commission

has charged nine firms with failing to disclose these conflicts of

interest. These actions included significant penalties against the

investment advisers, and collectively returned millions of dollars to

clients.

The reason this won't work is because there's no motivation to self-report. Advisers have to pay back all ill-gotten gains and admit to their customers that they mislead them, but the SEC won't impose a civil monetary penalty? C'mon.

Under the SCSD Initiative, the Enforcement Division will recommend

standardized, favorable settlement terms to investment advisers that

self-report that they failed to disclose conflicts of interest

associated with the receipt of 12b-1 fees by the adviser, its

affiliates, or its supervised persons for investing advisory clients in a

12b-1 fee paying share class when a lower-cost share class of the same

mutual fund was available for the advisory clients. Among other things,

for eligible advisers that participate in the SCSD Initiative, the

Division will recommend settlements that will require the adviser to

disgorge its ill-gotten gains and pay those amounts to harmed clients,

but not impose a civil monetary penalty. The Division warns that it

expects to recommend stronger sanctions in any future actions against

investment advisers that engaged in the misconduct but failed to take

advantage of this initiative.

Final thoughts: Initiatives like this are the reason why the SEC is absolutely ineffective.

___________

Finally, the Fed issued their weekly report on oil prices. It says that a "large drop in demand expectations decreased oil prices significantly". As a trader of crude oil, I know that the price of crude oil has gone nowhere but up since the middle of last year so I find this pronouncement humorous. Please note that gas prices are a key part of inflation. In fact, the Fed/FOMC credit low inflation with declining oil prices. In other words, the Fed is actively trying to suppress the true price of oil because. Final thoughts: The Fed's pronouncements are incongruent. The headline is the opposite of the points used to prove the point. The headline reads "Gas prices down", while the bullet points read, "Gas prices headed up." This is a classic case of someone being told what to say when they don't have the data to support the conclusion.

Many people are interested in cryptocurrencies, but are concerned about government intervention.

The SECs Chairman Jay Clayton made a statement about cryptos last month that was largely overlooked.

Clayton is doubling down on the “21(A) Report” at a time when his regulatory counterpart is embracing Bitcoin.

It appears a showdown is brewing: who controls the regulation of the fastest growing asset in the world.

I

enjoy talking to people about the viability of bitcoin. It appears to

have a different value proposition for everyone. For some, there is no

value proposition because they are certain

the government is going to shut it all down. These people are not

stupid — they know their government. For this reason, I think it’s

important to track statements made by government institutions like the

Federal Reserve and the SEC pertaining to Bitcoin, cryptocurrencies and

ICOs.

SEC Chairman Jay Clayton

On December 11, 2017, the SEC issued a statement regarding Bitcoin and cryptocurrency.

“This statement,” said SEC Chairman Jay Clayton sworn in by Trump in January of 2017, “provides my general views on the cryptocurrency and ICO markets…

Among the more interesting points Clayton points out in his statement are the following:

1) “to date no initial coin offerings have been registered with the SEC.”

2) “The

SEC also has not to date approved for listing and trading any

exchange-traded

products (such as ETFs) holding cryptocurrencies or

other assets related to cryptocurrencies.”

3) “If any person today tells you otherwise, be especially wary.”

Translation: The SEC has not approved any crypto or ETF.

“Please also recognize,” Clayton goes on to say,

that

these markets span national borders and that significant trading may

occur on systems and platforms outside the United States. Your invested

funds may quickly travel overseas without your knowledge. As a result,

risks can be amplified, including the risk that market regulators, such

as the SEC, may not be able to effectively pursue bad actors or recover

funds.

It

is Clayton’s job to protect investors, but I think he goes beyond that

role here. In particular, he tells investors to be weary because at any

point in time someone could run away with your money overseas — as if

this can’t happen with other investments.

This

is a specious argument. Your invested funds may quickly travel overseas

if you invest in stocks as well. In fact, they very likely do.

Corporations spend the money we invest with them overseas all the time,

why not? So yeah, this is a risk, but nothing we aren’t already very

much accustomed to with our current system of currency, which is over

90% digital.

On a good note, regarding ICOs, Clayton believes that:

initial

coin offerings — whether they represent offerings of securities or

not — can be effective ways for entrepreneurs and others to raise

funding, including for innovative projects.

So that’s good, but he goes on to say that:

replacing

a traditional corporate interest recorded in a central ledger with an

enterprise interest recorded through a blockchain entry on a distributed

ledger may change the form of the transaction, but it does not change

the substance.

Translation:

“The reason I like ICOs is because they’re essentially IPOs. If these

are really IPOs, I (the SEC) should be regulating them.”

Clayton

has two options regarding his views on crypto. He can say that ICOs and

cryptos are legal or illegal. Here Clayton does not mix words. He urges

market professionals to use a document referred to as (the “21(A) Report”) as legal precedent. The 21 Report is an investigative report released in July of 2017 in the SEC vs. The DAO.

the

Commission applied longstanding securities law principles to

demonstrate that a particular token constituted an investment contract

and therefore was a security under our federal securities laws.

He goes on to say that,

brokers,

dealers and other market participants that allow for payments in

cryptocurrencies, allow customers to purchase cryptocurrencies on

margin, or otherwise use cryptocurrencies to facilitate securities

transactions should exercise particular caution, including ensuring that

their cryptocurrency activities are not undermining their anti-money

laundering and know-your-customer obligations.

Or

what? This statement may sound threatening to those worried about

government intervention, but it’s more like the roar of a toothless

tiger. Money laundering disclosures are a joke in the financial

industry. Just during the week of Christmas, the Federal Register

announced that the Trump Administration would be waiving fraud and

corruption fines for Citigroup (5-year exemption), JPMorgan (5-year

exemption), Barclays (5-year exemption), UBS (3-year exemption), and

Deutsche Bank (3-year exemption). This is the same list of megabanks

that the Obama Administration extended one-year waivers to as well,

though it is

particularly troubling that Trump, unlike Obama, owes these banks a

large amount of money. Even if the exemptions weren’t in place, any

fines rendered are a tenth of a percent of the profits made. What’s

ironic is that the SEC has been rendered impotent over the last five

years by the very institutions that are asking for its protections

today.

What’s Next: Wall Street Is At Odds With Itself Over Bitcoin

In

my next article we’ll continue to look at the battle brewing between

the CFTC and the SEC. Both want control over this growing industry. On

the one hand government regulators like the SEC want to shut Bitcoin

down. On the other hand, the CFTC recently approved bitcoin futures

contracts for several institutions including the CME, CBOE and Cantor

Fitzgerald. Both sides have many stakeholders with deep pockets. My

money is on Bitcoin.

Disclosure: I am/we are long cryptos. I wrote this article myself, and it expresses my own opinions.

Bitcoin

Faucets like Cointiply are a great way to obtain cryptocurrency if you don’t have the

funds to invest in Bitcoin, but still want to invest in this growing

asset class. Who knows what Bitcoin will be worth in 7 years.

Below, I show you how to make the equivalent of $8K in bitcoin using Cointiply.

But first, let's do a quick primer of bitcoin faucets.

What are Bitcoin Faucets?

A “faucet” is a term used in the

cryptocurrency world. It means a place where you can go to claim a

small amount of crypto (like 1% of $.01). There are hundreds of faucets

out there. Some are scams, some (like Cointiply) are real.

At first I (like

many others) dismissed this as a Ponzi scheme. It isn’t. You are

investing your time, nothing else. Faucet owners get paid by

advertisers and in exchange they give you a portion of those earnings.

I’ve been doing it for about a month and have made a successful

withdrawal of coins to my wallet.

All you need to sign up for the

faucet is an email address and a computer. Never give your ID, address

or any payment information to any faucet.

Bitcoin Faucet Claims Are Small

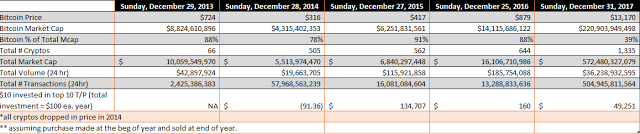

Early investors of Bitcoin paid just $.06

for a Bitcoin. A $100 investment seven years ago would be worth $28

million today. One year later at $3.19, $100 would have bought you 31

Bitcoin. In 2013, Bitcoin really took off to $724. In

June 2017, no one thought Bitcoin could go much higher than $2,500. At

the end of 2017, Bitcoin was trading for $13,170. Today it's trading for over $50K.

No wonder people are fascinated with Bitcoin as an investment.

The biggest complaint about Bitcoin faucets is that “the amount of the

claim is small.” If you are already wealthy or got in on

cryptocurrency 7 years ago, I can understand your concern. Bitcoin

faucets make small claims, but you never know where Bitcoin will be

trading in 7 years. Still, this is a valid concern, especially for

people with bills to pay and no extra time on their hands.

This is my response to these concerns:

1) The amount is small, but there are ways to maximize your earnings (I'll show you how to do this with Cointiply below).

Each faucet, like a game, has a few secrets that can greatly increase

your earnings, sometimes by 500%. I’ll explain the key to maximizing

your claim amount for each faucet in a moment.

2) You can’t

make a decent income by yourself, you need referrals. Those referrals

must be users as well. It is not enough to simply give someone else

your referral code. You also need to help them optimize the claim

amount.

3) Bitcoin is the front-runner in the fastest growing

asset class in the world. As you can see from the chart below: the

value of Bitcoin is highly volatile and tends to go up over time.

This is perhaps the most important aspect of this experiment for me.

It gives anyone with an email address the ability to earn/mine crypto,

just like Bitcoin miners were doing 7 years ago.

In one year

the value of the Bitcoin you have may be 10x what it is today. It could

also be 10x less, but at least you don’t lose any money if you “mined”

your Bitcoin from a Bitcoin faucet. In other words, the value of what

you hold may be small today, but the value of cryptos is going up and

if the trend continues, this is a way for you (for everyone)

to invest even if you don’t have the money. If you don’t have access

to your own computer, go to a computer lab or a library. Use your

phone. It’s also a great way to hedge against those dollars in your

savings. As the value of cryptocurrencies goes up, it will be against

the dollar.

Not all faucets are the same

Some faucets are definitely better than others.

With Coinpot gone, Cointiply has taken the lead as the world’s best bitcoin faucet.

What does it mean to be the “best” faucet — it means providing the best opportunity for higher and consistent payouts.

To figure this out, we need to create a model. The model is based on the following assumptions:

1 dollar = 10,000 Cointiply coins

1 Cointiply coin = $0.0001 dollars

1 bitcoin = 56,300 US dollars

1 bitcoin =563,000,000 Cointiply coins

Now let’s make some basic assumptions about your level of activity on Cointiply.

There’s the main faucet, which can be boosted by increasing your Cointiplier (we’ll talk about how to do that in a moment).

There’s also offer walls (visiting webpages, downloading apps, watching videos), surveys, videos, and paid to click ads.

You can also boost your earnings temporarily and permanently by playing the game Cointivity, which is a little mining game created by the folks at Cointiply (we’ll talk about this a bit later as well).

Last but not least, you can earn 5% interest on your balance if you have over 35,000 coins, which isn’t hard to do.

Let’s take a minute to model out how much you can make on each, starting with The Faucet.

The FAUCET

If you're new to Cointiply, start by signing up here, then make your first faucet claim by rolling the dice.This is the easiest way to make your first coin.

Cointiply has one of the best faucets out there. It’s attached to a progressive jackpot, which as of now is for 272,881 coins.

On average, I make around 30 coins per claim, but you can make anywhere from 22 to 280 coins. The amount depends on the roll.

For the purpose of creating a model, let’s assume you make 22 coins per roll and roll the faucet as often as the faucet allows (24 times a day or once every hour). If you do this, you will make 385,440 coins, $38.54 or 0.0006846181172 bitcoin in one year.

Seems small I know, but just wait.

Important: This is our baseline. I doubt you’ll be able to make a claim every hour on the hour, but you may also make more than 22 coins per claim, so it all evens out, especially because only a small portion of your payout is going to come from the faucet (unless you win the jackpot of course). The largest portion of your bitcoin will come from offers and maximizing those offers, which you’ll see in a minute.

Note: This baseline amount includes the loyalty bonus, which doubles your reward. You get a loyalty bonus of 1% for every day you make a claim on the faucet up to 100%. So as long as you make at least one claim per day, you will receive the loyalty bonus. Offer Walls

Cointiply offer-walls are a great way to earn coins. According to the website, top users earn 100’s of thousands coins from offer walls. The most popular offer walls are Theorem Reach, Tap Research, Adscend Media and Adgate Media. There are more than a dozen others. They are all different, so find one you like and work it. The good news is you have variety.

A single survey or offer can pay as much as 300,000 coins, with many paying between 1,000 and 20,000 Coins. There are many offers for both US and non-US players.

Tip: always click on “Earn Coins” first. You will see a list of the most popular offers as well as any new ways to earn additional coins.

Some offers are for games and others are surveys or simply ads to click on. Games and offers pay the most, while pay-per-click ads pay the least (9 coins per click). Cointiply paid-to-click ads are pretty normal. You earn coins for visiting a webpage and they’re available all around the world.

Watching videos is one of the most passive ways to earn coins because all you have to do is pull up a video and have it streaming. My favorites are VideoFox, EngagMe and Hideout.tv. You need to see 3 ads before your account will be credited. The same applies to Hideout.TV. You earn points for every three ads that play between videos.

For our earnings model, let’s say you can commit to doing four offers per month that average out to 50,000 coins per offer.

That’s a total of 2,400,000 coins per year or $240.

Now let’s add videos.

Let’s say you can commit to watching two hours of video every day. You don’t really have to watch, just have it on. You are allowed to watch video from three different portals (cell phone, desktop, tablet) at one time. For the purposes of this exercise, we are going to be conservative and just use one portal for 2 hours per day. That’s a total of 43,797 coins per year or $4.38.

Next: What if we add interest to our model?

Earning Interest

Cointiply pays 5% annual interest on coin balances over 35,000 coins.

To earn interest, you have to maintain this balance and make at least 1 claim each week.

To start earning interest, you need to go to the settings page and toggle the “Enable Interest” switch and then save your settings. Interest is paid every Sunday night.

As a word of caution, be sure to place a 2FA on your account if you have enough to earn interest. You can find the 2FA set up in settings.

Interest is calculated using an annual interest rate of 5% paid out once a week based on your average daily balance. For example, if you have 100,000 Coins for a 1 week period you will earn 99 Coins interest for that week (100,000 * 0.05126 / 52.14). Based on our numbers above (approximately 7,400 coins per week) that equates to 370 coins per year. Not much, but you don’t have to do anything for it.

Next: Now let’s look at how much we can make on offers, games, video and paid per click ads.

So where does that put us?

If we add offers, videos and interest to our annual tally we get:

2,831,958 coins

$283.20; and,

0.005030120818

Two things to keep in mind:

When we first started this project, bitcoin was worth around $10,000 so these numbers are not static. For example, bitcoin extraordinaire, the person that introduced me to bitcoin, Max Kaiser predicts bitcoin will be trading at $240K by the end of the year. So he’s predicting an almost 500% growth rate this year.

This amount is based on both conservative and aggressive assumptions.

So now that you know about all the ways to earn bitcoin on Cointiply, let’s talk about how you can boost earnings.

The Cointivity Game & It’s Impact On Earnings

This is perhaps the main reason I like Cointiply so much — there are so many ways to boost your earnings. The Cointivity Game gives you the ability to boost your earnings.

How much can it boost earnings?

The following is an overview of how much we’ve earned so far using the model:

As you can see, the largest percentage of your earnings come from doing offers. So you can really maximize your earnings by doing two things:

Increase the number of offers you do from once per week to every day.

Boost your earnings potential on the day that you do those offers by purchasing “items”.

If we increase the number of offers per week from once per week to seven per week, we can increase annual earnings from $283 to $1,724.

Cointivity Maximization Strategy:

Select one day a week to do all 7 offers and then purchase items that boost earnings for that day.

To understand this, first a little tutorial on how to purchase items.

CointiPoints are Cointiply’s reward point system. For every 10 coins you earn , you’ll receive 1 CointiPoint. The more Cointipoints you have, the higher your level. You can also use these points to buy “items”. The “items” are used for your “bitcoin mining business”.

The goal is to collect as many items as possible to be successful with your bitcoin mining business. However, you can only collect items if you have a “slot” to place the item in.

Each level you go up unlocks more “slots”, which allows you to have more items.

Now, let’s figure out what kind of “items” you can place in your slots.

Items: Equippables Vs. Consumables

Everyone starts off with 2 slots: 1 for Consumables and 1 for Equippables. Every time you unlock another level, you also get more slots to put your items in. Remember, you want lots of items because they boost your earnings, but you have to have slots to place them in.

There are two types of “items” that you can buy to help your mining business: Equippables and Consumables.

Consumables are items that are consumed or used in a short period of time. They are short-term in nature and the earnings boost from consumables is temporary.

Equippables are items that are part of your equipment. They are long-term in nature and they boost your earnings permanently.

Each item is also classified as Common, Uncommon, and Rare quality. Rare and Uncommon items boost your earnings higher than Common items.

Where can you find items?

In Pods. You can buy Pods with either CointiPoints or coins. Every Pod contains three items. The higher quality the Pod, the higher your chance of getting Uncommon and Rare items, which are worth the most.

In these Pods you will find “items” like the ones below.

We’re not done. There are also Cointivity Collections.

Cointivity Collections

Cointivity Collections are a way to get an even higher earnings boost. This is a great way to maximize earnings if you know you’re going to be on Cointiply for 4 to 72 hours.

Each collection requires a different group of items. The most valuable Collection also has the most Rare and Uncommon Items. Here’s a graphic from the website of the Collections currently available:

When you have all items in a Collection, a “LOCK IN” button appears on that Collection. Click the button, and you will be asked to confirm that you wish to activate the Collection.

TIP: If you know you’re going to have a big offer day, you might want to Lock In your Collection on the day before and then activate it on the day you are going to do the offers.

All of your items are part of your “Inventory”. So, at any point in time you can check to see how many items you have by clicking on Inventory. You can check out your level, your boosts, your slots, and the items you have in those slots by clicking on your Cointivity Profile. Also remember, that you can use the items to boost earnings or you can sell them for coins.

Let’s get back to maximizing strategy.

Our model assumes that on the day we complete 7 offers, we also purchase:

three Equipables that permanently increase the offer reward by 2% each

two Consumables that temporarily increase the offer reward by 3% each

one Collectible which temporarily boosts my offer account by another 7%.

By doing this I can increase annual earnings from $1,724 to $2,147.

If we assume that Max Keiser is right, and bitcoin is going to grow by another 500% by year end, the amount could increase to $8,000 by the end of the year. And that’s just in 1 year!

Two more things before I send you off to start your bitcoin mining business — Chat Rain and Cointiply Multiplier.

Next: Chat Rain

Chat Rain

Chat Rain is an opportunity to make a portion of the Chat Rain pool. I’ve never made much on Chat Rain, but I want to include it here even though I don’t include it in the model because you don’t really have to do anything for it.

At the top of the Cointiply Chat forum is a water drop icon, along with how many coins are in the current Rain pool. Cointiply does not tell you how big the Pool needs to be before it “rains”, but you can see what your current share is by looking at the Progress Bar. When the Rail pool is paid out, the site literally rains. The rain looks more like snowflakes than rain, but it’s cute.

The amount you can make depends on how many coins you earn for that day. The more you earn, the higher your share of the Chat Rain pool. You can also donate to the Rain pool, but it doesn’t increase your share so I don’t know why people do it. Karma? Important: You have to opt in to the Chat Rain pool by clicking on the “Tap to Qualify for Rain Pool” button.

Next: Cointiply Multiplier

Cointiply Multiplier

I’m not a big fan of gambling, so I didn’t mention this in the opening remarks. You want to earn and hold (or hodl as the bitcoin community likes to say). That said, if you’re into this for the gambling, you can wager as few as 10 coins or as many as 50,000 coins in Cointiply’s multiplier game. The maximum multiplier is 61.3x so you could make as much as 613 coins from a 10 coin wager, but it’s highly unlikely.

When you start a new round of the CointiPly Multiplier you will be presented with 11 different “targets” on the screen. The targets look like small white circles. If you win, you can either press your luck or play it safe and click the “Take Win” button at any time to claim your coins and end the round. What’s Next

I’ll be researching the impact of referrals and premium memberships on earnings.

Final thoughts: Crypto is For Everyone

The

world of investments is largely cut off from people that don’t have the

means, but crypto isn’t. I have family and friends on both sides of the

wealth spectrum and this is a great way for both to accumulate coins.

Those that have money, but are worried about Bitcoin’s viability, can

use faucets as a no risk way to participate in the crypto boom. Those

that don’t have the money can also use this as a way to participate.

Translation:

If you don’t have $1 million (or even $10,000), Cointiply is a great way

to earn crypto.