In The Last 12 months Our Strategies Have Made Over $2.7M Based on Backtest Results

We

all want to believe there’s a way to measure the forward strength of a

model, but as we’ve explained before, market data is not random. It is

based on auction mechanics. So, the same tools we use to validate and

test the quality of data in a random data set can’t always be applied to

the market. This is why we say ‘don’t use the simulated data feed within Ninjatrader’. It’s a random, internally generated market and has no correlation to real market data. So what can

you do? The best you can do is make predictions about the future based

on strategy performance and then track that performance, as well as the

rationale for your predictions, over time.

Last

week we published the results from a backtest of all strategies on the

E-Mini Russell 2000 (RTY). We then compared those results with the

E-Mini NASDAQ 100 (NQ) backtest. There were some interesting

observations that you can read more about here.

In that post we talked about the impact of volatility on trading profits. We also reviewed the definition of volatility:

“A measure of dispersion around the mean.”

…and,

discussed what our next steps were in the process: namely to compare

our backtest results with other assets. In particular, those assets that

may be more volatile than indices, like commodities.

If forced to label myself, I would say that I'm an egalitarian. I believe that each person has the right

to live life in any way they choose as long as it doesn't hurt or infringe upon the rights of others.

Do unto others as you would have them do unto you.

It's a deceptively simple doctrine to live by, because it takes strength to see yourself in the next man when he can't see himself in you.

While I believe in local government, I also believe that like Gollum's precious ring, power corrupts. It turns God's best into greedy little trolls and makes it easier for the next man to dismiss you as being beneath him. And, while a federal government may seem like a progressive next step, it is actually antithetical to the movement started by the libertarians and egalitarians that created the ideal of America. None of us, including them, ever lived in its ideal -- a place where all men are created equal, endowed by their creators with certain inalienable rights, among them, life, liberty and the pursuit of happiness.

Can you imagine thinking that our leaders were taking steps to secure our happiness? It is unimaginable to most, but the founders of this country took the first step. They stepped on the ideal of others to create it for themselves, but it was created nonetheless and we are, for better or worse, who we are because of it. Either way we have a debt to pay and it cannot be paid in dollars. It must be paid by your own pursuit of liberty and justice for all.

Money and freedom are not the same

It is wrong to believe that money and freedom are the same. The brainwashing begins early on in life, so it's hard to decouple the two, but you don't need money to gain your freedom. In fact, the pursuit of money is often at odds with your freedom. You don't need capital for liberty. Liberty is an unalienable right endowed upon us by our creator(s). And, if our creator(s) bestowed it upon us, why let a man, or even a nation led by a man, take that unalienable right away.

So I fight for liberty for all. These aren't mere words -- they mean everything. They can seem lofty and ephemeral, but there are ways to anchor them to reality. The best way to do this is by asking the right question with every action. Is your goal to be rich or free? Do you strive for acceptance or freedom? Do you worship the dollar or liberty?

Many good people are conflicted by these questions and with good reason. What good is liberty if your child is hungry? It is this fear that causes delusional thinking. Instead of logic and reason, we turn to whatever works, which usually doesn't.

The beautiful thing about the system we live in is that there are many options. It may feel as though your path is pre-defined, but this is yet another delusion. In reality, your options, from minute to minute, are unlimited. And, you don't have to quit your day job to choose a different path.

The right path begins with the right question

José Clemente Orozco's painting, The Demagogue

I’m a big fan of Elon Musk. In an interview about how he and his team

tackled challenges when creating Tesla, he lamented, "A lot of times

the question is harder than the answer. If you can properly phrase the

question, then the answer is the easy part." I like this quote because

it exposes a truth that we often get wrong—finding your holy grail in life (whatever that may be) is about asking the right questions. If you ask the right questions, the answer will come.

Musk

recalls that his first questions as a founder were pretty mundane,

like, how can I make enough money to live and still have time for games

and computers? His first few companies, like Zip2 and X.com, were

designed to make money. As he got more money, he got frustrated with how

money was transferred, and that led to PayPal. Today, the market cap of

Tesla is around $40 billion and SpaceX is estimated at $15 billion. As

Musk's founder questions have gotten better, his companies have gotten

bigger. "To the degree we better understand the universe, then we know

which questions to ask," he says.

Elon’s

first question was “how do I make money”, but he didn’t start

making real money until he asked the question “how can I make transferring

money easier?” The answer to that question was Paypal and the rest is

history.

So, the right question is not:

How can I make more money? (wrong)

It is:

How can I get more freedom? (right)

Another question I used to ask myself was:

Which political party should I donate to? (wrong)

But the real question to ask is:

How can I create real change in my neighborhood and beyond? (right)

I haven't voted in an election for many years. I believe in mutual aid, not electoral politics. I donate to the People's Party and Jimmy Dore, but that's it. Any other donation goes straight to the people in need and the people most in contact with those people.

Take the time to learn more about where you buy groceries. Is it a corporation or employee owned? Before supporting your favorite brands, find out if their employees are on strike and why. If you have the luxury, as much as possible, make your purchase decisions based on liberty rather than the lowest price and our collective freedom will come.

Every

two months we like to look at how our top automated trading strategies

are performing and update you on our key findings, highlights,

takeaways and what’s in the pipeline. Externally, it tells you where we

are and allows subscribers to give their input. Much of our research has

been a derivative of subscriber inquiry.

Internally, we are

looking at two things in particular — alpha decay/consistency of

published strategies — what can this tell us about the best strategy

attributes and how can we use these attributes together to create a

strategy that gets us closer to the holy grail of trade strategy. We

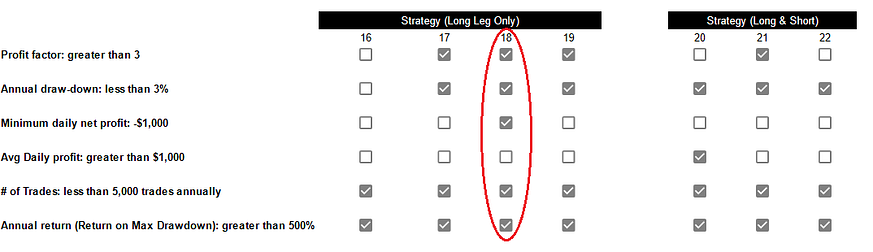

define the holy grail of trade strategy as having the following

attributes:

Profit factor greater than 3

Annual drawdown less than 3%

Annual return greater than 500%

Minimum daily net profit of -$1,000

Avg Daily profit greater than $1,000

Less than 5,000 trades annually

Greater than 500 trades annually

Notice

that we’ve added another bullet — the strategy has to produce more than

500 trades per year. We’ve noticed that strategies that produce less

tend to have inconsistent backtest results.

We’ve also added two

columns to the end of the backtest table - cumulative low and cumulative

high (see below). Instead of just looking at the lowest and highest

daily net profit, we wanted to look at the cumulative high and low over

the year. While this is highly dependent on when you start the strategy,

when combined with profit factor and max drawdown, it can provide a

compelling risk/reward profile.

For example, Strategy 28has

the lowest daily cumulative profit at $9,690, which means that even

though the strategy had a max drawdown of $16,365, the total account

value never dropped below $9,690 on a rolling or cumulative basis. Yes,

this means that on day 1, the strategy made $9,690. Again, this has more

to do with when the strategy is started than profitability, but it can

make all the difference in the world, especially with a highly volatile

strategy. This is the main reason we include profitability per day of

week and hour of day in our strategy results. We’ll discuss this more

later.

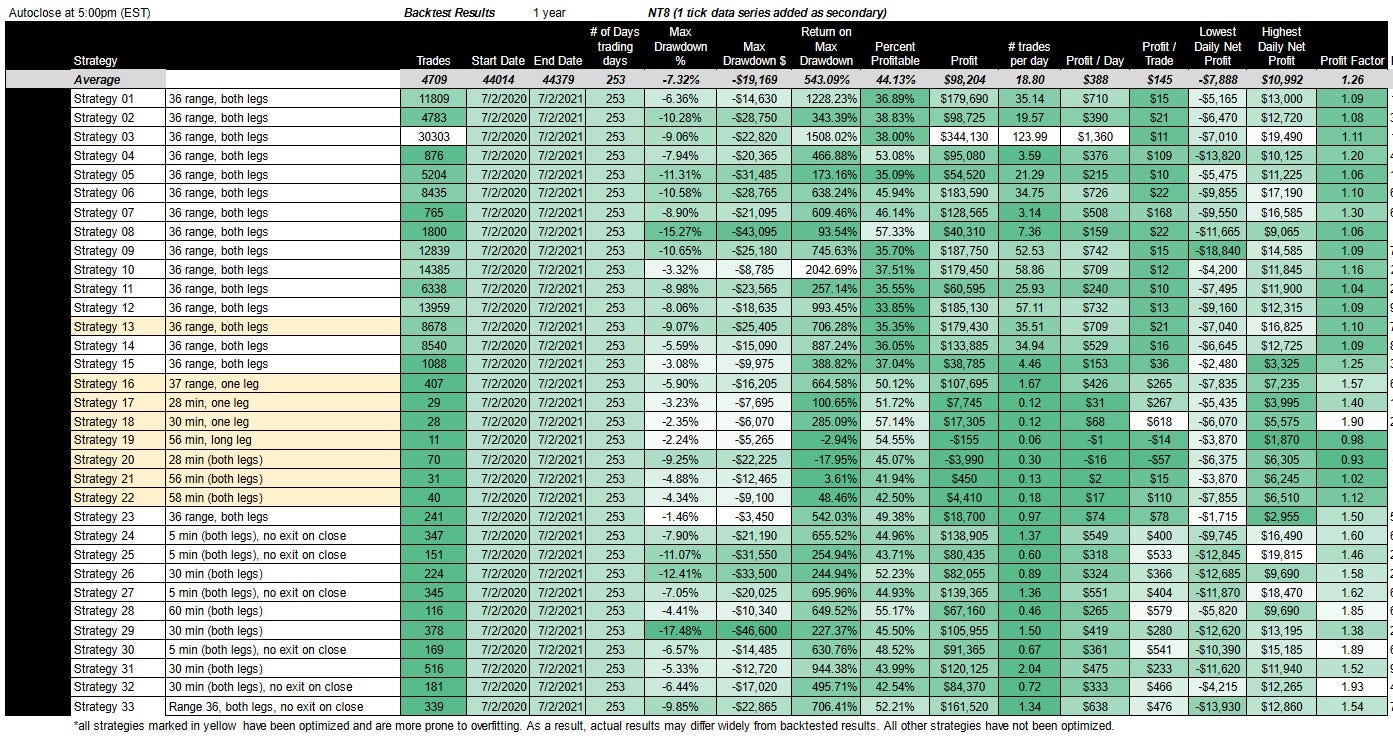

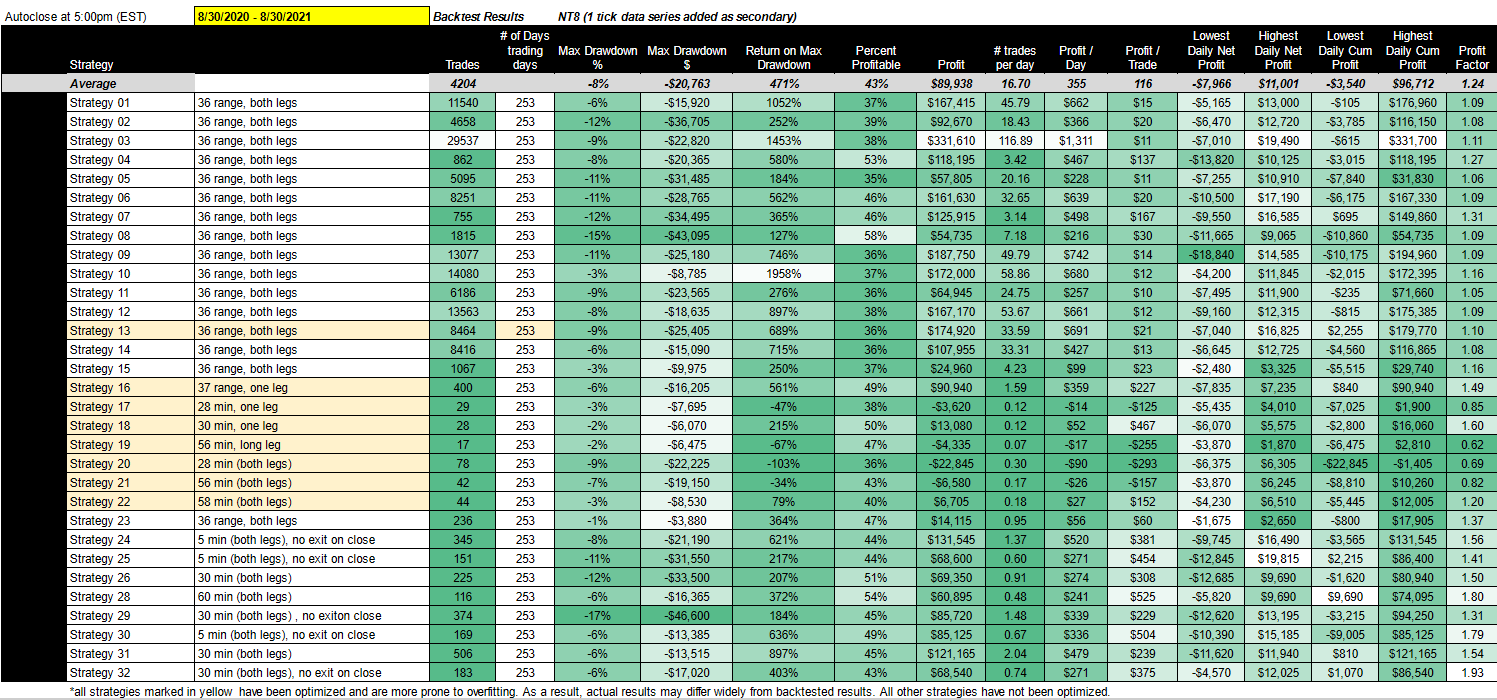

7/2/2020 - 7/2/2021 Vs. 8/30/2020 - 8/30/2021

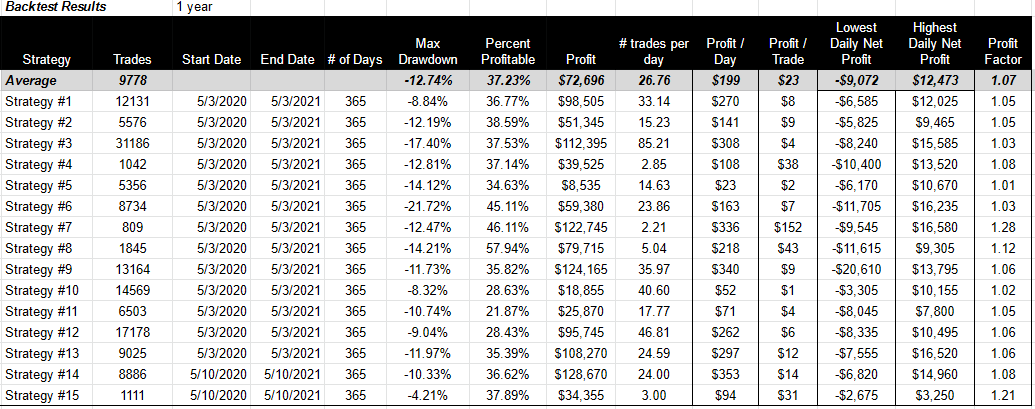

So where do we stand in comparison with our last update? The table below provides the backtest results from our last update: 7/2/2020 - 7/2/2021

The following table provides the backtest results for the current or most recent update: 8/30/2020 - 8/30/2021

[Our apologies for the small font, but you can enlarge by clicking on the picture.]

In

general, when comparing the performance of both time periods, we had

the same drawdown as the last update and a slight decrease in the return

on max drawdown due to a decline in profitability. Average profit

factor for the entire portfolio decreased from 1.26 to 1.24 and average

net profitability decreased from $98K to $89K. Profit per day decreased

from $388 to $355 and profit per trade decreased from $145 to $116. The

number of profitable trades also decreased slightly from 44% to 43%.

Most

of the deterioration occurred with optimized strategies (marked in

yellow on the chart). Optimized strategies are more prone to overfitting

and therefore have highly inconsistent results.

So what happens

if we remove all optimized strategies from the portfolio? The chart

below provides a comparison with and without optimized strategies.

Profitability

increased from $89K to $110K on average. Likewise, average profit

factor increased from 1.24 to 1.30, profit per day increased from $355

to $436, and; profit per trade increased from $116 to $155.

What

does this tell us? Optimized strategies do not work, at least using the

methodology we’ve used in the past — almost all optimized strategies

performed worse except for Strategy 22. It also tells us that our unoptimized strategies are performing well against the previous update. Strategies 4, 7, 8, 10, 11, 26 and 31 all performed better. Strategies 4 and 26 had the highest increase in profit factor.

For

the year, net profit for the total portfolio increased from $2,223,095

to $2,788,075 with a total max drawdown of $643,640. Specifically, the

model is telling us that a $643K investment could have made $2.8 million

between 8/30/2020 - 8/30/2021. This amount does not include

commissions. We advise a fixed price commission plan for strategies with

more than 1 trade per day.

The biggest question, or the question you should be asking yourself, is how can I guarantee this will happen again next year? Unfortunately, the answer is you can’t and don’t believe anyone that says that you can. All

we can do is track how these strategies perform over time.

Specifically, we are looking for consistency over time, which is why we

conduct an update every two months like the one you’re reading now. We

continue to mine and isolate the attributes of our top performing

strategies with consistent results. The goal is to take the best

attributes from the best performing strategies to create the holy grail

of trade strategy.

We recently published a post titled: Top 5 Strategies By Performance. It gives an overview of the top 5 strategies in each category. This is a summary of the post:

Strategy 3 has the highest net profitability at $331K.

Strategy 3 has the highest profit per day at $1,311.

Strategy 8has the highest percent profitability at 58%.

Strategy 10 has the highest return on max draw at 1958%.

Strategy 23 is the only strategy with a drawdown of less than 1%

Strategy 23has the lowest daily net profit at $1,675.

Strategy 25 has the highest daily net profit at $19K.

Strategy 25 has the highest daily cumulative profit at $331K.

Strategy 28has the lowest daily cumulative profit at $9,690.

Strategy 28has the highest profit per trade at $525/trade.

Strategy 32 has the highest profit factor at 1.93.

Subscribers, click here

for a link to a discussion on how we used these top strategies to mine

for the specific attributes that make these our best strategies.

What’s in the pipeline:

Much is in the pipeline.

We recently published a post titled: Do our strategies work on cryptocurrencies?

In general, one of the most common questions we get pertains to the

use of our strategies on other assets like crypto, so we’re also going

to publish backtest results for other asset classes, including stocks.

We’re also looking at various data series types outside of ‘range’ like minute, tick, volume and Renko. Subscribers can click here for the full post on our experience with Renko backtest results.

Another

commonly asked question is in regards to overfitting. You can read the

following posts to learn more about overfitting and what we’ve done to

reduce its impact: Overfitting: What is it and what can we do about it and What Are We Doing To Ensure Backtest Accuracy?

After writing these posts, we became interested in creating a strategy

that optimizes in real time. That is, instead of optimizing a strategy

in 1 year backtest results, and then using those results as a way to

place parameters on the future, we can optimize a strategy as close to the event as possible.

In this way, the optimization is still based on backtest results, but

the data used in the backtest is based on a very short period of time.

Theoretically, overfitting should be less of a problem the closer the

optimization occurs to the event. We’ll be publishing information about

this indicator shortly.

We also plan on publishing a follow up post on market structure. We received some great feedback on this post and we’re hoping to incorporate it into our regular analysis.

We continue to receive questions about the difference between Total Investment & Reinvestment: This is our answer: Reinvestment Vs Total Investment.

In addition, we’ve just added cumulative net profit to our table as a

key performance indicator. When used in conjunction with max drawdown

and return on max drawdown, you can get a better understanding for how

much you’ll need to invest/reinvest in a strategy. Some of our

strategies have positive cumulative net profit, meaning that the account

value never drops below 0. We take a deeper look at these strategies in

the post: Top 5 Strategies By Performance Indicator.

There

are several other posts in the works, but it would take too long to

discuss them here. Some research has been delayed and some has been

pushed up. If you have any questions about anything in particular,

please reach out to us directly.

The market is based on auction mechanics. This is why prices aren’t random.

An

auction is a system of buying and selling goods or services by offering

them for bidding—allowing people to bid and selling to the highest

bidder. The bidders compete against each other, with each subsequent

bid being higher than the previous bid. Once an item is placed for sale,

the auctioneer will start at a relatively low price to

attract a large number of bidders. The price increases each time

someone makes a new, higher bid until finally, no other bidders are

willing to offer more than the most recent bid, and the highest bidder

takes the item. -Corporate Finance Institute

This

is the nature of a simple auction, but this isn’t how the futures

market works. In a futures market the auctioneer is on a never ending

search for price discovery.

The futures market is actually the

result of tulip auctions conducted by Dutch traders in the 1600’s. They

wanted to buy and sell tulips year round, not just for 3 months of the

year. This is the beginning of what is known today as the Dutch Auction.

A Dutch Auction is when the auctioneer starts with a high asking price and lowers the bid until one of the bidders accepts the price. Items for sale are allocated based on the bid order: the

first highest bidder picks their items, followed by the second highest

bidder, and the third highest and so on. Dutch auctions are often used

for commodities and investment securities. Alphabet (Google) had a

famous example of a Dutch Auction —Google’s Dutch Auction.

So

what? This means that in a Dutch Auction new information can come in

and change the direction of the market at any time. This new information

acts like a wind that changes the direction of the price wave.

So, in a Dutch Auction, new information isn’t immediately digested into the market — it is a process that is based on bid order and that process usually plays out in threes. First,

you will see an initial push or “price attempt” to change the

direction. The first move is the initial test and is followed by a

pullback. Then you will notice a second attempt, which I like to refer

to as the bandwagon trade. Then there’s the last movement before the

price moves in the opposite direction. The price will continue to trend

in either direction until it finds equilibrium.

This is the

framework or template for price discovery in the futures market. The

variables that impact this process the most are speed (tick per second)

and volume or market depth. So, if you had to create a formula for the

best conditions to trade it might look something like this:

Where

price potential is the potential change in price, speed of price is

measured as ticks per second, market depth is measured in terms of

volume expansion/contraction and market divergence is measured as

(number of contracts traded / number of orders). Keep in mind, there

will always be more contracts traded than orders because traders often

trade more than 1 contract. We are currently in the process of

developing a strategy that makes use of this formula as a way to define

the best time to trade. We’re also using it as a barometer for knowing

when to “flip” the strategy (make the opposite trade).

In

general, the higher the potential, the better the trade. Low potential

is marked by quick pullbacks and choppy markets. High potential is

marked by strong price movements. Those movements can be either sideways

or trending up/down. They can also be tracked by lines referred to as

“trend” lines. If a price is trading within known trend lines it will

hit a price on the line and then go the other way. In other words, the

lines act as support and resistance for the price. When the price is

pushed outside of these lines, it is referred to as a breakout.

Breakout Trades

You

can confirm that new information has entered the market with breakout

activity. It is also marked by an expansion in volume as well as an

increase in the speed of the market. The best way to take advantage of a

breakout is by tracking the trend line. When the price breaks above the

trend line, you’ve got a breakout, which means new bidders/seller have entered the room and have changed the direction of the trend. In general, breakouts only happen 1 out of 3 times that a price hits the trend line.

So

the market is a combination of trends and breakouts. And these trend

line and breakout attempts are patterns that repeat over and over again.

You can find this structure (3 movements) at every time frame of the

market. If you drill down, you’ll find it at the 1 minute or 150 tick

level. If you drill out, you’ll find it at the 15 min or 5,000 tick

level. The same patterns exist at every level of the market. In this

way, the market moves like a fractal. That is, it creates a pattern that

repeats on itself. One of the best Youtube videos that explains this is

below.

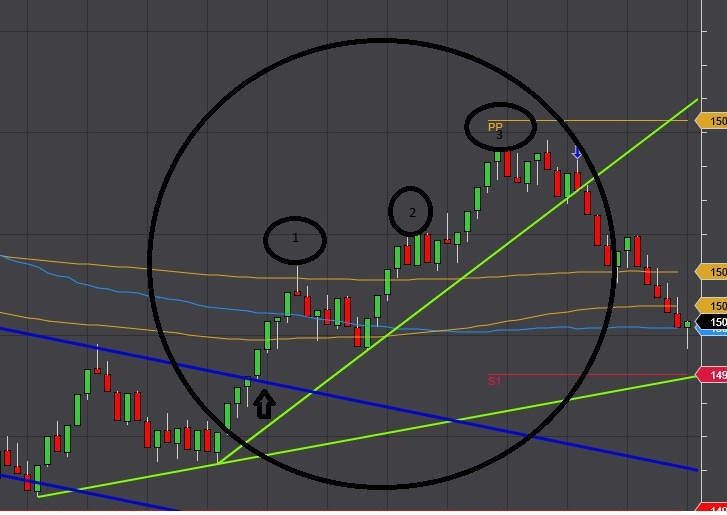

The point is, you will find the same patterns at the 36 range level that you will find at the 18 range level.

Here’s an example of a 36 range chart and 3 price movements marked as 1, 2 and 3.

The

trend line marked in light green supports all three movements. The

price finally breaks below the trend line in a downward move. The

movement starts with an upward breakout from a downtrend (marked by the

blue trend line). If you’re a subscriber click here for instructions on how to use our favorite trend line indicator.

The

chart above is a 36 range chart and the chart below is an 18 range

chart. Specifically, this is a price chart of the first movement in the

36 range. It has three movements within it. And, if you look closely,

you will see that the first movement in the 18 range also has three

movements within it. Again, the market is a fractal.

This is a common pattern in trading due to auction mechanics.

From

a candlestick perspective, this is referred to as the three bullish

soldiers — each bar going higher than the last. To those that follow

candlestick patterns, this is a very bullish signal.

And

then of course there’s the great Richard Demille Wyckoff — one of the

most well known traders in history. In the early 1900’s, Wyckoff

developed a strategy around market mechanics and named each segment of

the trade (1, 2 & 3) Spring, Throwback and Correction.

From

a market mechanics perspective these movements are marked by an

accumulation and distribution phase — accumulation leads to an increase

in price while distributions lead to a decrease in price. Wyckoff’s book

is still taught on Wall Street because market structure is a function

of the underlying dutch auction. You can view a pdf of his original work

on the Internet Archive by clicking here.

How Can We Use This To Help Us Find The Holy Grail of Trade Strategy?

We

are still on the hunt for the holy grail of automated trade strategy.

If we apply the rules of market structure, we can use it to look for two

events that are certain to happen:

1) bandwagon movements

2) breakouts

Like

most strategies, we are searching for an event that takes place within a

condition and then we to need to define the action to take within that

event. In this case, the event is a bandwagon movement or a breakout and

the action is a buy or sell order with a trailing stop and possibly a

limit order on entry. The trick (or the part we’ve failed at thus far)

is to define the conditional that describes the price action just before

the bandwagon movement or breakout occurs.

To learn more about who we are and our quest for the holy grail of trade strategy, click here.

A

common question we get is, ‘do you teach’? The answer is no. None of us

have any interest in teaching at the moment, but we can give you a

recommendation. If you’re interested in learning more about futures

trading or automated trading we recommend taking classes from Quantra.

They’ve been around for over 10 years and have a mix of free and paid

classes. Before signing up for anything, however, check out the

credentials of Quantra’s faculty and compare it to other online schools.

You’re looking for a mix of academic, practical, and institutional

experience.

First, happy reconstitution day traders! This is often the heaviest trading volume day of the year and this year it’s happening today (June 25). Get ready for a wild ride this afternoon. Click here to read more about what reconstitution is and how it impacts trading.

Second, there’s a mechanical elephant in the room and it’s called “overfitting”.

We

aren’t programmers, statisticians or mathematicians in any way. So, we

have to translate many of these terms into something that makes sense

to us from a trading perspective.

In a nutshell, the definition of

overfitting is: Good performance on backtested data, bad performance on

future data. Specifically, it’s when a strategy learns the “noise”

that’s specific to the backtest period, but that noise does not apply to

future data.

So, the question is: what is noise in

trading and how do you know the difference between a strategy that has

been “overfitted” to the backtest data, but won’t perform well in the

future and a strategy that performs well in backtests as well as in the

future?

This is what we’re hoping to answer with this post.

Trading is both art and science

An illustration from Jules Verne's novel "The Steam House" drawn by Léon Benett.

I

could limit this discussion to what we’re doing to prevent overfitting,

which I do below, but I think it’s also important to understand how it

applies to trading.

This is not an easy topic to discuss,

primarily because the market is dynamic — statistical tools are not a

fan of dynamic. Likewise, any attempt to forecast the market requires

both art and science. Overfitting may explain why simple models don’t

work in the future, but it has limitations on models that are dynamic

and influenced heavily by outside forces, also referred to as noise.

I

was amazed by how much literature there is on the topic of overfitting.

It is of particular interest to those in the simulation or machine

learning space, which makes sense. These strategies can be viewed as

bots or machines and the holy grail of trading strategy is a bot that

has “learned” the market. To do this, the bot would have to “learn” how

to treat noise. Is it good noise or bad noise? This is where the comparison breaks down. Eliminating the noise in trading is extremely difficult because the market is primarily a reaction to noise, but we may be able to discern the good noise from the bad.

What does this have to do with overfitting? Overfitting happens when a model learns the detail and noise

in the historical data that negatively impacts the performance of the

model on new data. We know that we can optimize a strategy that then

performs poorly in the future, but does it perform poorly because it

learned the noise or because the noise is unlearnable? The only

thing that’s truly learnable is the ability to identify the ideal

conditions for a strategy to operate in. In other words, we’re looking

for a strategy that knows when to trade. We can’t control the market,

but we can control when the strategy takes action. The result is a

strategy with fewer false flags (carving out the gross loss) and a

higher profit factor.

So on one hand we can use the

concept of overfitting to understand why a strategy does not perform

well in the future, but on the other hand we must admit that the concept

has limits for something as dynamic as market structure. It is almost

impossible to not engage in overfitting when developing strategies, but

there are things we can do to minimize it.

What can we do?

I

want to go back to the original question. How are we making sure that

our strategies aren’t the product of overfitting and will continue to

do well in the future?

Optimize on hyperparameters one at a time

- When we make changes to a strategy we make them one at a time rather

than optimizing several variables at the same time. This gives us an

opportunity to isolate the benefit of each change to net profit and

profit factor.

Change the conditions of the strategy, not the hyperparameters:

We don’t just want to create the machine, we want to change the

surroundings or the environment of the machine. We want to create

resistance to overfitting within the strategy itself. Put yet another way, we want to create the machine and

define the conditional path it takes within the strategy. By doing so,

we aren’t as concerned with the hyperparameters as we are the conditions

of the strategy. For example, we aren’t as concerned with optimizing

the hyperparameters of MACD (slow parameter, smooth, and fast) as

much as we are with creating a condition that triggers an action (MACD

cross when volume is higher than 3000). The trader can then update the

volume accordingly rather than the hyperparameters of MACD. Volume sets

the condition. In this way, the holy grail could be a moving target.

Focus on scenarios rather than sensitivity

- This piggybacks on the above. We’re more interested in creating an

environment within the strategy. This environment is like a scenario

(mid day, low volatility, low volume) rather than a single variable. So,

while we optimize based on one variable at a time, the conditions

within the strategy are based on a scenario.

Use two sets of data in the backtest:

Going forward, in addition to doing what we’re doing now, we’d like to

use two sets of historical data, one to optimize on and one to test on,

both are part of historical data. We’re thinking of using 3 months of

validation data for the test along with a 3 month break. So that’s 18

months altogether. We’ll use the first 15 months in the backtest,

followed by a 3 month break and then use the next 3 months as a test in

two different data charts. This format may change, but this is the

current plan.

Use Gross Loss/Profit in the calculation of Profit Factor

- We use gross loss and profit rather than a variant that uses average

loss and profit when calculating profit factor. The average ratio may

smooth out the impact of big winners and losers, but that seems to lend

itself to overfitting, especially since this is one of the primary

performance measures we track and optimize on.

Use more than one instrument in backtest data - As a final check, we’re going to start running strategies through other instruments such as ES, GC, BTC, YM and stocks.

We’re

hoping that these actions will help to ensure we’re picking up the

“good” noise and not the noise that’s specific to a particular day or

time frame when optimizing on backtests. That said, some of our

strategies have no optimization at all and our focus is still heavily

concentrated on NQ for its volatility.

Conclusion

I

believe the market is full of both random and definitive events. Some

things you do every day, some things are random (you know you eat lunch

at around 12pm, but you don’t know what you’re going to eat). Like a

simulation, everything is interconnected and random in the market and

yet if you span out far enough some predictions can be made. It is this

fractal nature of trading that makes it so interesting. The conundrum in

trading is that the further you span out (i.e. increase the time

series) the more susceptible you are to risk; the more predictable the

market is, the more risk your trades carry. The predictable part of

trading is the science (indicators, etc) and the unpredictable part is

called noise. Indicators act different based on the noise. For example,

most indicators are highly predictable in a rally, which is why traders

love a good rally. So perhaps the best course of action is to create a

strategy that is only triggered during a rally. This is much easier said

than done, but just saying it gets us closer to the goal.

Trading

is both art and science. Some of the most seminal papers in economic

theory use formulas filled with assumptions that don’t make any sense

(i.e., symmetry of information — an investor will never have access to

the same information that a corporation would and investors will rarely

behave rationally). These assumptions hold no relevance now, but they

were used as a way to create a science out of economic theory and that

science has little real world application. So it’s important to use

statistics to track and measure progress and performance, but it’s also

important to realize that statistical tools have a limit. Newton had to

create the mathematical form we call calculus to express the laws of

physics. Likewise, it could be that forecasting market structure

requires a completely different way of thinking about “learning”,

especially when the prevailing analytical framework dismisses relevant

data as noise. As a result, data scientists are quick to blame poor

performance on noise, but if we’re looking for a mathematical formula

that can predict the true nature of the market it must include the

noise. It isn’t that thinking about the market from a statistical

perspective is bad, but it can limit our visibility and therefore our

ability to find the holy grail of trade strategy if we get too attached.

Ultimately, while there are several key takeaways from

this discussion, the main one is that not all noise in trading is bad.

The key to discerning the good from the bad isn’t about changing the

actions of the strategy, but the environment that those actions are

taken in. And, we’re finding that those strategies that control the good

noise through conditional equations and data series calculation

(minute, range, tick, etc) seem to do better in the future.

What’s In The Pipeline?

There’s

a lot in the pipeline, but we’re prioritizing something rather big

right now. We’ve been impaled by a unicorn in the past, so we’re doing

some due diligence before sharing, but the preliminary results are

phenomenal. We want to say thank you to Pierre, one of our subscribers,

for making a research request that has the potential to improve all of our strategies. Again, we’re compiling the data now and will share as soon as we feel it’s been properly vetted.

Happy trading!

To read more about our Automated Trading Strategies click here.

To subscribe to the Automated Trading Strategies newsletter click here.

Gustave Doré’s illustration to Orlando Furioso: a knight and his men see a knight and lady approach in the forest

I recently wrote a post titled: We Are Treasure Hunters Searching For The Holy Grail Of Automated Trade Strategy. I asked readers to “join us in the hunt for the holy grail in the dark and scary forest”. Moments later I received an email from a subscriber that seemed distressed. He was upset because he felt we were encouraging people to invest in automated trading strategies that were based on simulated data. He didn’t feel our assumptions were correct and seemed to question our motives. So I want to use this post to be clear about our goals. I also want to tell you a bit more about my personal background and what we envision for this newsletter.

Our goal:

We are hunting for the “holy grail of trade strategy” and we define that strategy as having the following performance:

Profit factor: greater than 3

Annual draw-down: less than 3%

Annual return (Return on Max Drawdown): greater than 500%

Minimum daily net profit: -$1,000

Avg Daily profit: greater than $1,000

# of Trades: less than 5,000 trades annually

Where do we stand today?

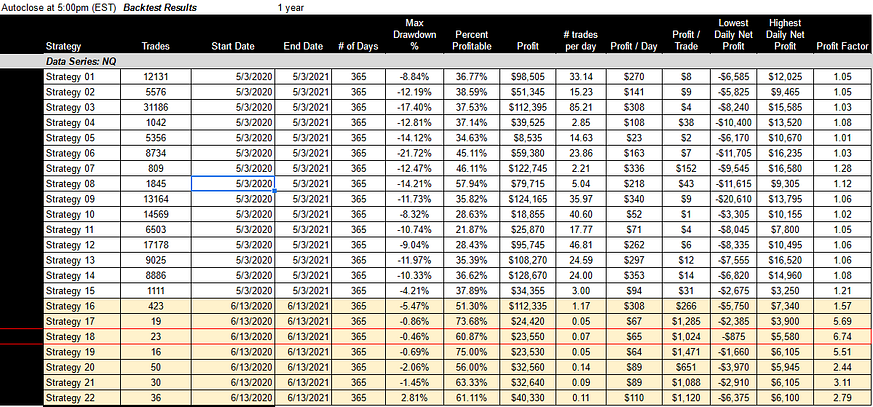

We have 22 strategies listed so far per the chart below and we try to post at least one strategy per month.

We haven’t found the holy grail yet, but we’re getting close:

As you can see Strategy 18 is our rising star. It has 5 out of 6 of our criteria and a profit factor of 6.74, which means that it made 674% more in gross profit than gross loss last year. (members click here for a description of Strategy 18)

This is one of the primary objectives of Automated Trading Strategies: to find the holy grail of trade strategy. Our subscription fuels that research and we share all trade strategies that come out of this research with our members. To be clear: our paid subscription is specifically for those that want to share in the product of our research.

You don’t need to invest real dollarsin our strategies to join the hunt

We want to encourage people to join us on the hunt for the holy grail of trade strategy. That said, and this is very important, you don’t need to invest real dollarsin our strategies to join the hunt. You don’t even have to subscribe to our newsletter to join the hunt.

We are targeting three groups of people with this newsletter:

Novice or New trader — Someone interested in trading

Seasoned Trader — Seasoned trader looking for an edge in a new strategy; automated or not

Automated Trading Strategy Hunter — Looking for high performing automated trading strategies and research specifically aimed at increasing the performance of trading strategies in general.

Within these groups, there are those that want to use our strategies live and there are those that don’t.

This section is a must read for those that want to use our strategies live.

We welcome and encourage all three groups to use our strategies, but it is important to keep the following things in mind, especially before going live. We are speaking to the novice or new trader, the seasoned trader and the automated trading strategy hunter:

If you can’t afford to lose your full investment, don’t trade — not just our strategies, but in general. Automated trading is specifically for people that can afford to lose the full investment. At a minimum you’re going to need the annual draw-down on net profitability to get started. In other words, if you lose this money, it’s not going to result in a change in lifestyle. I have followers that are constantly on the lookout for alpha. Their threshold is low due to low/negative rates on fixed income products. These are the same people that drop $25,000 on doge and then sell it when the price pops to clear $4 million. I personally gave away over 50,000 doge on Medium (when it was trading for $.0000005) so this is a real phenomenon.

Don’t ever go live on any strategy (ours or anyone else’s) without testing it first. We’re giving you a map, but you need to vet it out. Go on the trail yourself, GoogleMap it, think about how much food/drink you’ll need along the way, what kind of supplies — develop a game plan. Even then, the weather (market) may change on the day of the planned hunt, so nothing is guaranteed (more on this later).

There are trading costs that are not included in our published stats, i.e. broker commissions, data costs, slippage, platform costs, research, internet, equipment, taxes. These costs depend on the trader/asset so you should think about what the cost of each is to you and what impact that has on net income. This is why you want a strategy with a profit factor (ratio of gross profit over gross loss) greater than 1. This is also why we report net profit per trade — all of these costs can be calculated at the per trade level.

I’ve said this before, but it makes sense to repeat myself here, we are day traders, not coders or financial engineers. We’re a bunch of old day traders with little technological experience. We like to drink and talk about the markets on Friday afternoon. I don’t personally trade any of our strategies with real dollars, only simulated live. As a day trader, I make 1–2 live trades per day with a 3/5 to 1 risk reward ratio. And, I’ll continue this until I find an automated strategy that offers the same risk profile.

Trading is hard

One common question we get is, ‘if I don’t know how to trade, can I still trade your strategies?’ Before I tell you the answer, I want to tell you about one of my favorite shows — Alone.

Alone is a reality TV show about a group of people that compete to see who can survive in the wilderness alone for the longest period of time. The winner gets $1 million. It always amazes me when contestants show up on Day 1 with absolutely no knowledge of basic survival skills. But every season there’s the idiot that could barely make it past one night. There’s also the guy/gal that hunts for a living, studies bush-craft, is a religious fan of the show and has already developed a daily game plan based on the success of winners in past seasons. Rarely is his/her motivation about money; it’s about the psychological challenge, the love of the hunt.

Trading is the same way. It’s hard and you have to be prepared. You have to love the markets. You have to submit to the trend and create a game plan for defeating the dragon (your ego). It isn’t about the money; it’s about the psychological challenge, the love of the hunt and a fascination with market structure. So I would say using our strategies to trade if you don’t know how to trade is only preparing yourself to be eaten. Otherwise, you’re the idiot that signed up for a survival show that doesn’t know how to survive.

And, what’s nice about trading is that if you’re good, the market will provide — there’s no need to sign up for a contest.

Love at first sight

Personally, I’m in love with trading — I’ve been hooked ever since we first met. I try to convert friends and family, especially those with with kids and grand kids (simulated trading is basically a video game and kids love video games). Once you start making money in a simulated environment there are several companies that will fund you after passing a test — just do a search for funded trader programs.

While trading in a simulated environment is akin to playing video games (you haven’t really risked anything but time), it can help to hone your skill-set to a point that you go on autopilot when trading live. It takes a lot of practice to learn something at the subconscious level. Indeed, it is said that it takes 10,000 hours of trading to make money.

As a day trader myself, I can attest to the hours required to learn how to trade. I’ve been trading for many years. I started as an associate working for a major investment bank. My job was to get prices for exotic currencies with no market so it was more about relationships than market knowledge.

I worked on the bank’s trading floor. This was when institutional traders played poker and drank beer at lunch; they kept a 25 year-old bottle of Glenfarclas under the desk and a bottle of 222s in the drawer. They were the wildest people in the bank and they always got free stuff from brokers. One weekend a broker sponsored a “trader’s only” weekend at the Ritz. I had the time of my life.

We all wanted to be the head trader. Bank leaders loved them. Risk managers feared them. They were unfettered, unruly, untouchable and I wanted nothing more than to be one of them.

I was a junior trader on the FX desk at the time. I didn’t know it, but I had one of the best mentors in the business. Back then, we had a squawk box that connected us to other traders, but sites like Oanda.com were just getting off the ground and traders were just starting to realize the implications that came along with financial technology. This was about the same time that banks started bringing in quant savants and financial engineers to create automated strategies. Traders knew that everything was about to change. And it did. Some traders stepped out on their own and lost it all. Some made fortunes.

What did I do?

This is my story

I opened an account with $10,000 and lost it all in nine days. I had no one to complain to, no one to blame. I could have blamed my mentor for laughing at me when it happened, but that’s what he was supposed to do. I was the only one to blame.

$10,000 was a lot of money for me in those days. I entered into a deep depression. Within days of entering the dark and scary forest I’d been eaten. A feral dragon came out of nowhere and devoured me head first. I tried to get away, but there was no reasoning with the creature — I was standing in some sort of emotional quicksand. (It seems obvious now, but I was the dragon)

This is when I decided to do two things:

Develop an impenetrable risk management plan for day trades

Create automated trading strategies

I needed something that would take the emotion out of trading. I needed something that would help me to slay the dragon — better yet, I needed something that would help me to avoid the dragon altogether. And so I began my own little hero’s journey. I haven’t stopped. Along the way, I found others. There are many others.

We’ve all been eaten.

We’ve all sacrificed.

We’ve all suffered.

So I understand when traders, especially those with experience, get mad when they feel as though other traders aren’t explaining the risks of trading to newbies with adequacy. Some traders are just selfish and want to keep the profession to themselves, but others are genuinely concerned. When we bring people into the dark and scary forest they can get eaten and we don’t want to be responsible for that. That said, for some hardheaded idiots (like myself) being eaten is part of the initiation.

The goal of any legitimate mentor isn’t really to teach you how to trade, it’s to teach you how to minimize the risk of being eaten. The more analytical you are, the harder it is to slay the dragon. Good teachers measure their success by the number of students that are still alive at the end of the day. While there are no guarantees, there will always be another trading day. So, the first question you need to ask your mentor is: What’s your risk management plan?

There are no guarantees

There is no guarantee that any strategy (simulated or live) will produce the same result in the future. We know and believe this. But, we also believe our requirements for the holy grail of trade strategy will point us toward a strategy with a true edge in the market. Furthermore, we believe that edge will be large enough to make up for any deviation that’s not modeled out in the simulation.

What’s Next:

All Subscribers: Next Strategy Update/Review coming up on July 6

Members: We are currently focusing on strategies involving pattern recognition. We would like to combine pattern recognition with reversion to the mean theory (Strategies 16–22 in particular) to see if an opportunity exists to increase net profitability.

On 7/8/2021 our subscription price will be going up. You can read more about that here.

Research Requests For Members: Thanks again for all the great questions and our apologies on the delayed response for some. Current research requests include:

Do our strategies work on cryptocurrencies (this is a common question)?

Are certain trading days better for automated strategies (earnings season, economic data releases, FOMC announcements, triple witching hour). If so, can we take advantage of these days in the future?

What can market physics/auction mechanics tell us about trading strategy?

Can we develop a strategy that does better in the lunchtime lull?

Can we develop a strategy that does better during morning volatility?

Can we combine lunchtime lull and and morning volatility strategies into one?

If you have any questions, please reach out to us directly at automatedtradingstrategies@substack.com.

We (Automated Trading Strategies) recently received a question from a subscriber regarding total investment. He wanted to know how much a trader had to invest in each strategy (see a description of all strategies here), not just net profit.

In other words, if we find a strategy that makes $100K a year, how much did it take to make $100K in one year? Did it take $50K or did it take $1 million? Due to the nature of futures trading, the answer can be both. We’re going to take a few minutes to explain why that is in this post.

Reinvestment Vs Total Investment

Any good automated or algorithmic trade is going to move like the market, which tends to ebb and flow. Very rarely is the market direct in its path to a particular point of support or resistance. So it is not unusual, especially for automated trades that use indicators as a trigger to buy and sell, to have high reinvestment.

Some traders view reinvestment cost as the cost of doing business, it’s almost impossible for a day trader not to. You use your account size, which for me is only 2% of $50K on any given day, to make more profitable trades than unprofitable trades. If you make $200, that’s great. $200 is your net profit, between your gross loss and your gross profit, but this doesn’t tell you how many trades it took to get there. It could have taken 11 trades with a gross loss of $1,000 and a gross profit of $1,200. So you lost $200 on 5 trades and made $200 on 6 trades, which put you up $200 on the day. Your gross loss is $1,000 and your gross profit is $1,200 — net / net you made $200 on the day.

One way that traders measure reinvestment is with the profit factor. Profit factor is the ratio of gross loss and gross profit. Going back to our example, if you’re up $200 after losing $1,000 and making $1,200, the profit factor is 1.2 (1,200 / 1,000). So your breakeven is 1 or $1,000.

Let’s kick it up a notch

What if you made $200,000 for the year off of a gross profit of $2,200,000 and a gross loss of $2,000,000. Net/net, you’re up $200,000 for the year. Does this mean you have to have a $2,000,000 account to trade? Not at all. Gross profit and gross loss are like the notional rather than actual market value of your trades. It’s important, but not nearly as important as the incremental wins/losses.

That’s why we use draw-down as a measure of the % of cumulative profit that has to be used in the reinvestment rather than the % of the account size or gross p/l. So when we say that the draw-down is 20%, using our example, it means we had to give back as much as $40,000 of the $200,000 cumulative profit made over the last year. The higher the draw-down, the higher the capital requirement.

We prefer to measure capital requirement in this way because it takes daily reinvestment into consideration.

So it’s not wrong to focus on net profit rather than gross profit/loss. Indeed, a good automated trade strategy has its eye on both.

The Holy Grail of Trade Strategy

As a quick reminder, our goal is to find the holy grail of automated trade strategy and we think we can find it faster together.

We’ve defined the holy grail of trade strategy to be the following (based on annual performance):

Profit factor greater than 3

Annual draw-down less than 3%

Annual return greater than 500%

Minimum daily net profit of -$1,000

Avg Daily profit greater than $1,000

Less than 5,000 trades annually

We have yet to find this illusive trade strategy, but we’re on the hunt!

If you subscribe to our newsletter, you’ll be among the first to find out when we do.

Note that we’ve included a requirement for a profit factor of 3.

We believe automated strategies with a profit factor of 3 and higher weed out strategies that aren’t efficient. It’s like an ROA (return on assets) of sorts. Investors like Warren Buffet look for high ROA investments because they make more money per dollar of invested assets. Rather than simply comparing earnings to the number of shares outstanding, or price to earnings, Buffet compares price to the dollar value of assets used to get you to that price. Put another way, instead of looking at earnings potential, Buffet looks at asset potential -- does the price of the investment correlate with the underlying investment in assets. Likewise, we are looking for strategies that create 3x more gross profit than loss.

The end result is an optimization of profitability -- automated strategies that stand the test of time.

The Key To Maximizing Profit Factor

So what is the key to maximizing profit factor?

Answer: Minimizing gross loss.

Based on the work we’ve done so far, the key to minimizing gross loss is to decouple complementary trades. In other words, just because you go long on an upward cross, doesn’t mean you have to go short on a downward cross. You can go long and then exit the long. And/or, you can short and then exit the short. Then you can put a strict conditional around each leg. In other words, you can isolate the profitable trades within the strategy. We found that this greatly increases the profit factor.

This is the first of a series of posts based on research requests

submitted by subscribers of Automated Trading Strategies. Our goal is to find the holy grail of automated trading strategies.

We’ve defined the holy grail of trade strategy to be the following (based on annual performance):

Profit factor greater than 3

Annual drawdown less than 3%

Annual return greater than 500%

Minimum daily net profit of -$1,000

Avg Daily profit greater than $1,000

Less than 5,000 trades annually

We have yet to find this illusive trade strategy, but we’re on the hunt! If you subscribe to our newsletter, you’ll be among the first to find out when we do.

While we share our answer with all

subscribers, only paid subscribers can request research.

This subscriber wanted to know what the impact of optimizing strategies based on time period would be.

Before answering this question, I want to explain how we compare results with the chart below. I also want to explain what the Profit Factor (last column) is.

Profit Factor

Here’s a chart showing the performance of our strategies over the past year.

Please

pay close attention to the profit factor in the last column. This is

our primary performance indicator. One of the main goals of this

publication is to find a strategy with an annual profit factor greater

than 3. We refer to it as the holy grail of trade strategy.

Profit

factor is a function of gross profit and loss. It is the ratio of the two.

So when gross loss equals gross profit we have a profit factor of 1.

One

thing we’ve learned after running hundreds of strategies through

simulation is that most strategies trend toward a profit factor of 1. In

a nutshell, this is because the markets tend to revert to a mean.

Intuitively,

it isn’t surprising to learn that when strategies are linked together

by an indicator, they tend to have a gross loss and a gross profit that

are remarkably similar over a 365 day period. So then the question is:

Is

it possible to identify, isolate and reverse portions of gross loss. If

we can’t reverse the loss, maybe we can just eliminate the bad trade

altogether. This brings us back to time.

What Does Profit Factor Have To Do With Timing?

Timing

is an aspect of the trade that we can isolate. We can find the hours of

the day, in general, that the trade is most successful and only trade

those hours. We can even optimize just one leg of the trade.

So, we optimized all our strategies and this is what we found:

In

general, the profit factor (gross profit / gross loss) increased by

15-25% when we optimized the strategy based on the strategy’s most

profitable trading hours.

The impact was particularly high for the long leg of the trade.

To

be clear, reducing the time period reduces net profit, but increases

gross profit compared to gross loss. The end result is a strategy that

is more efficient and reliable allowing you to increase your contract

size over time.

What’s Next

Now that we know that timing can increase the profit factor by 15% to 20%, we want to continue our research by researching reversion to the mean theories.

Specifically, we want to know:

If profit margin on all strategies tends to trend toward 0 or a profit factor of 1, is there a way to capitalize on this truth?

Is it possible to achieve a higher profit factor using strategies based on reversion to the mean theory?

As an example, we are currently looking at implementing mean reversion indicators like Bollinger Bands into our automated trade strategy and will share those strategies with subscribers of Automated Trading Strategies when complete.

– painter (Mexican) Born in Jalisco")